MossConsulting • SmallBusinessTax • TaxSeason • BusinessFinance • HRHelp • PayrollTips • FICAExplained • PayrollTaxes • May 4, 2026 10:41:11 PM • Author: Nicole Moss

Payroll taxes are the part of running a business that nobody gets excited about - but getting them wrong is one of the fastest ways to end up with IRS penalties, cash flow problems, or both.

The good news is that once you understand the components, the math is straightforward. This cheat sheet breaks down every payroll tax you need to know, with real numbers and practical examples.

The Two Sides of Payroll Taxes

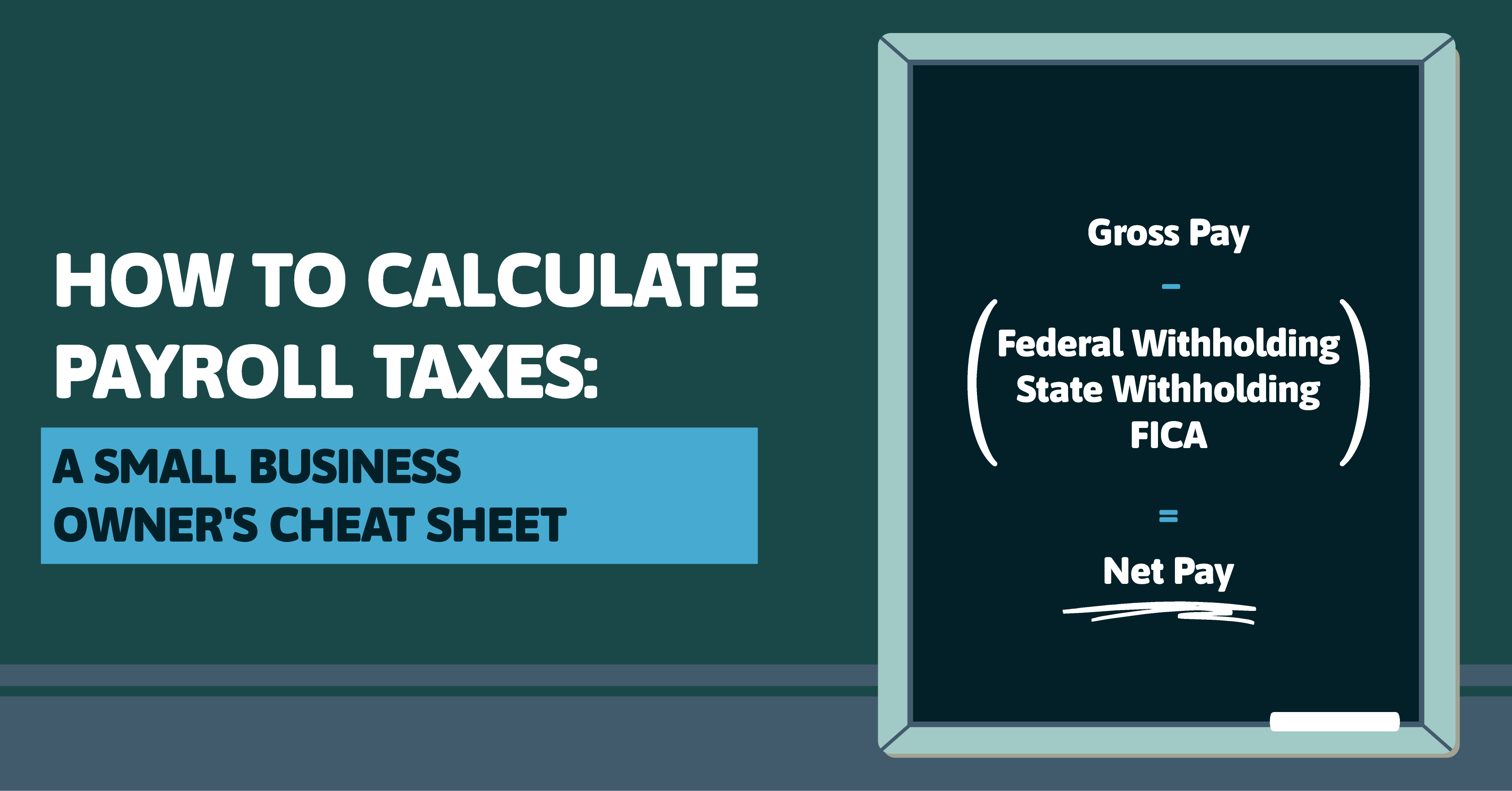

There are taxes you withhold from your employee's paycheck (they owe these, you just collect them), and taxes you pay as the employer on top of what you pay the employee. Both must be deposited with the IRS on schedule.

Employee-Side Withholdings (You Withhold From Their Pay)

Federal Income Tax: The amount depends on the employee's W-4 and how much they earn. The IRS publishes withholding tables each year that tell you exactly how much to withhold per pay period. This is not a flat rate - it's based on their filing status, dependents, and any additional withholding they've requested.

Social Security Tax: 6.2% of gross wages, up to the annual wage base limit (currently $168,600 for 2024 - check IRS.gov for the current year's limit). Once an employee earns above that threshold, you stop withholding Social Security for the rest of the year.

Medicare Tax: 1.45% of all gross wages. Unlike Social Security, there's no cap. Additionally, employees who earn above $200,000 in a calendar year are subject to an additional 0.9% Medicare surtax. You don't match this extra amount - it's employee-only.

State and Local Taxes: These vary widely. Some states have no income tax. Others have flat rates or progressive brackets. Some cities and counties add local taxes on top. Check your state's department of revenue for current rates.

Employer-Side Taxes (You Pay These On Top of Wages)

Social Security Tax (Employer Match): Another 6.2% on the same wages, up to the same annual limit. This is your cost - it doesn't come out of the employee's check.

Medicare Tax (Employer Match): Another 1.45% on all wages. Again, your cost.

Federal Unemployment Tax (FUTA): 6.0% on the first $7,000 of each employee's annual wages. However, if you pay your state unemployment taxes on time, you receive a credit of up to 5.4%, reducing your effective FUTA rate to just 0.6%. For most employers, that means you'll pay $42 per employee per year in FUTA.

State Unemployment Tax (SUTA): Rates vary by state and are based on your industry and claims history. New employers typically start at a default rate, which adjusts over time based on whether former employees file unemployment claims. Rates can range from less than 1% to over 5% depending on your state and experience rating.

A Quick Example

Let's say you have an employee earning $50,000 per year, paid biweekly. Their gross pay per period is $1,923.08.

For each pay period, you'd withhold federal income tax (based on their W-4 and the IRS tables), Social Security at $119.23 (6.2% of gross), Medicare at $27.88 (1.45% of gross), and any applicable state/local taxes.

As the employer, you'd also owe a matching $119.23 for Social Security, $27.88 for Medicare, and FUTA and SUTA on the first $7,000 of their annual wages.

The total employer cost of payroll taxes on a $50,000 salary is roughly $3,825 to $4,500 per year, depending on your state. That's an additional 7.5% to 9% on top of the salary - and it's a number every business owner should budget for from the start.

When to Deposit

The IRS assigns you a deposit schedule based on your total tax liability. If you reported $50,000 or less in taxes during the lookback period, you deposit monthly (due by the 15th of the following month). If you reported more than $50,000, you deposit semi-weekly. New employers typically start on a monthly schedule.

Late deposits trigger penalties that escalate quickly: 2% for deposits 1-5 days late, 5% for 6-15 days late, 10% for more than 15 days late, and 15% if not deposited within 10 days of an IRS notice.

Quarterly and Annual Filing

Every quarter, you'll file Form 941, which reports total wages paid, taxes withheld, and your employer share of taxes. This is due by the last day of the month following the end of each quarter (April 30, July 31, October 31, January 31).

At year-end, you'll issue W-2s to every employee by January 31 and file Form 940 for your annual FUTA reporting.

The Bottom Line

Payroll taxes aren't optional and they aren't flexible. Budget for them from day one, deposit on time, and keep clean records. The math itself is manageable - it's the deadlines and compliance details that trip people up.

If payroll taxes are taking up more of your time than they should, we can help. Whether you need a full payroll setup or just a second set of eyes on your current process, that's exactly what Moss Consulting does.