Offering a 401(k) used to feel like a big-company move. The setup was complex, the costs were high, and the administrative burden was real.

That's changed significantly - thanks to the SECURE 2.0 Act, new technology platforms, and a growing recognition that retirement benefits are one of the most effective retention tools available.

If you have fewer than 100 employees, setting up a 401(k) is now more affordable - and more beneficial - than it's ever been.

Why Offer a 401(k)?

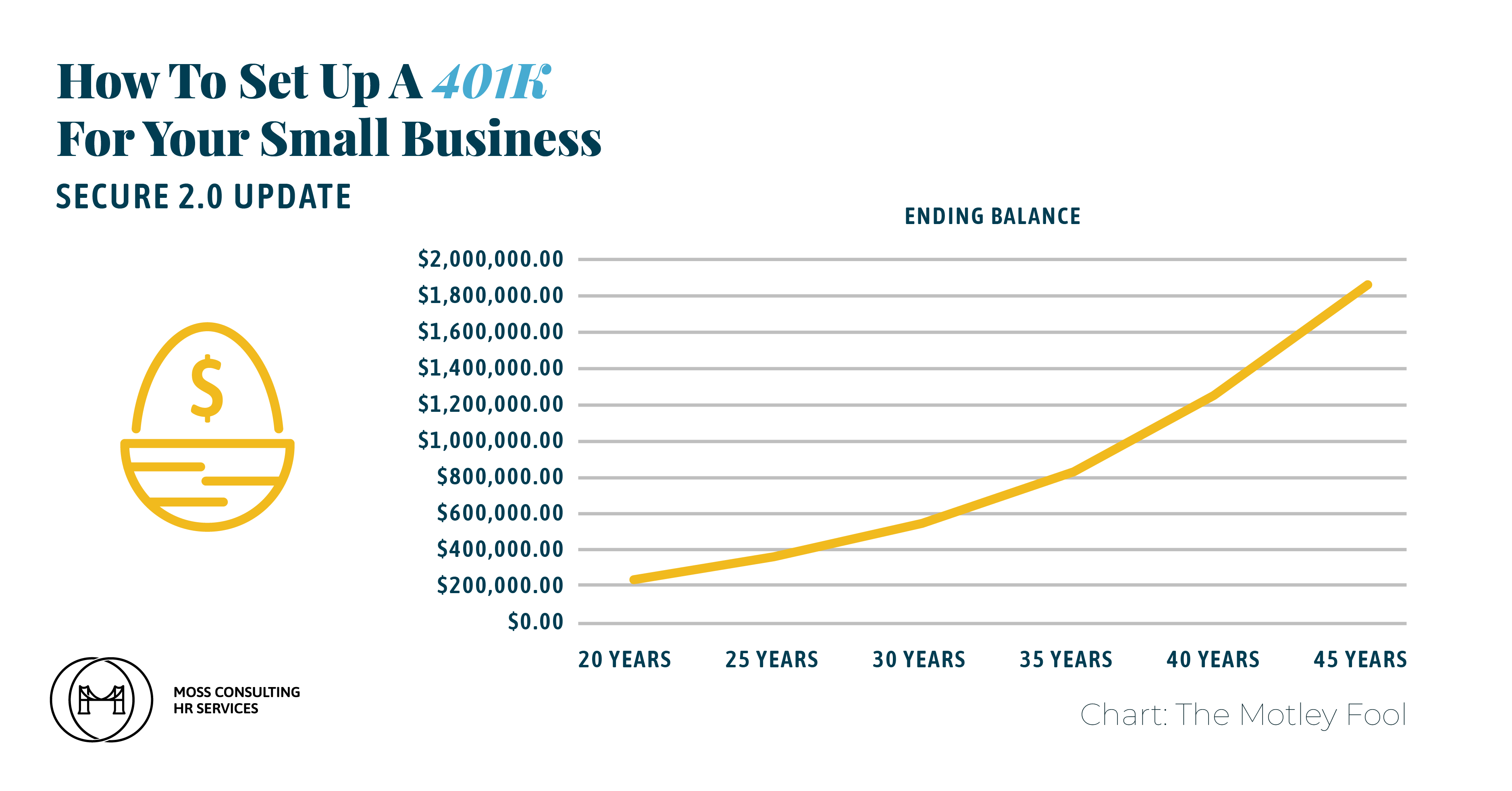

Seventy-four percent of employees say retirement benefits factor into their decision to stay at a job. For small businesses competing against larger companies for talent, a 401(k) can be the differentiator that tips the scale.

Beyond retention, offering a retirement plan signals that you're invested in your team's long-term wellbeing. And thanks to recent tax changes, the financial cost to your business may be lower than you think.

SECURE 2.0 Act: What Changed

The SECURE 2.0 Act, signed into law in December 2022, introduced several provisions specifically designed to make retirement plans accessible to small businesses.

Startup Cost Tax Credit: Employers with up to 50 employees can claim a tax credit covering 100% of plan startup costs, up to $5,000 per year for three years. Employers with 51-100 employees receive a partial credit.

Employer Contribution Credit: A new credit covers employer contributions for the first five years of the plan - up to $1,000 per employee per year. This phases out for employers with 51-100 employees.

Automatic Enrollment Incentive: New 401(k) plans started after December 29, 2022 are generally required to include automatic enrollment. While this sounds like an added burden, it actually increases participation, which improves plan health and can reduce per-participant costs. Businesses with 10 or fewer employees are exempt from this requirement.

The Setup Process

Choose a plan type. Most small businesses choose a Traditional 401(k), which allows both employee and employer contributions with flexibility in plan design. SIMPLE 401(k) plans are simpler to administer but have lower contribution limits and require employer matching.

Select a provider. Look for a provider that specializes in small business plans and offers transparent fee structures. Common options include Guideline, Human Interest, Fidelity, and Vanguard. Compare setup fees, per-participant costs, investment options, and the level of administrative support included.

Design the plan. Key decisions include whether you'll offer an employer match (and at what level), what the vesting schedule will be, which investment options to include, and whether you'll enable Roth (after-tax) contributions.

File with the IRS. You'll need to adopt a written plan document and file Form 5500 annually (small plans with fewer than 100 participants can file the simplified 5500-SF).

Communicate to employees. Roll out the plan with clear, simple communication. Explain how to enroll, how matching works, and why it matters. The more employees understand the plan, the more they'll participate.

Costs to Expect

Typical small business 401(k) costs include a setup fee (often $0-$500 with modern providers), monthly per-participant fees ($4-$10 per employee), and investment management fees (built into fund expense ratios, typically 0.05%-0.50%).

After applying the SECURE 2.0 tax credits, many small businesses effectively pay nothing out of pocket for the first three years.

Common Concerns (Addressed)

"It's too expensive." With the new tax credits, plan costs can be fully offset for businesses under 50 employees. Run the numbers - you may be surprised.

"It's too complicated." Modern providers handle most of the administration, compliance testing, and filings. Your time commitment is minimal after setup.

"My employees won't use it." Auto-enrollment addresses this directly. When employees are enrolled by default, participation rates typically exceed 80%.

Ready to Explore?

If you've been putting off a retirement plan because it seemed too complex or too costly, the landscape has shifted in your favor. We can help you evaluate providers, design a plan that fits your business, and take advantage of every credit available.

mossconsulting.com/book-a-free-consultation